Explainer

How to Automate Email Nurturing: Benefits and Setup (2026)

See the benefits of email automation for customer nurturing, from better segmentation and timely follow-up to clearer funnel tracking and stronger sales.

Payment processing with automated onboarding matters because every disconnected application, follow-up message, approval update, and billing handoff gives a merchant another opportunity to stall or disappear. The problem is not merely administrative delay. A merchant that never completes onboarding cannot process transactions, generate fees, or become an active account.

In 2025, Fenergo reported that 70% of surveyed financial institutions had lost clients because of inefficient onboarding, up from 67% in 2024 and 48% in 2023; average abandonment was approximately 10% (Fenergo, 2025 Financial Crime Industry Trends Report announcement). The survey covered 600 senior decision-makers, so the figures describe a broad operational problem rather than a single implementation.

A controlled onboarding workflow connects the merchant application to outreach, document collection, review, activation, and recurring billing. It does not remove underwriting judgment. It removes the copying, chasing, status checking, and repeated data entry surrounding that judgment.

We have worked through this exact handoff problem with service businesses whose contact records, approval decisions, and invoices lived in separate systems. The recurring pattern is that the individual tools work, but nobody has defined the state changes connecting them.

A dependable onboarding workflow coordinates the full merchant lifecycle while keeping approval and risk decisions under authorized human control.

- Automation should move records, not make unsupported risk decisions.

- The workflow needs explicit statuses, owners, timestamps, and exception states.

- Approval is not the finish line; activation and recurring billing must start correctly.

- Success should be measured through response, completion, activation, payment, and exception metrics.

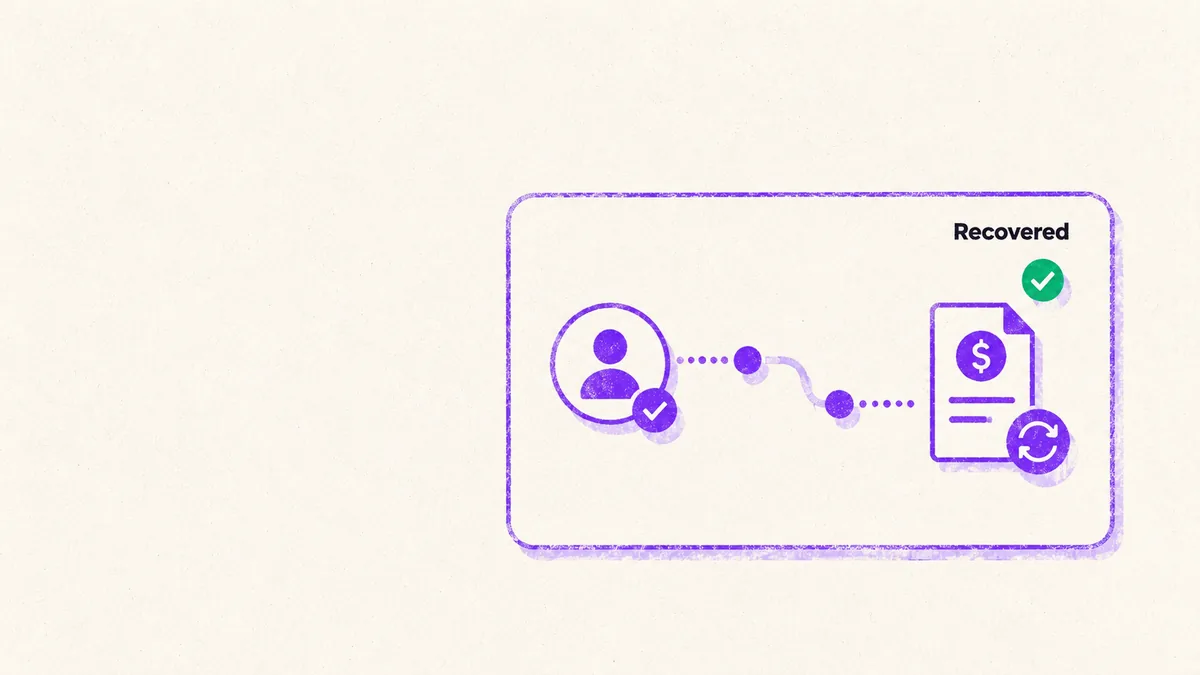

- In a Stripe customer case study, automated recovery later reclaimed 48% of revenue associated with failed charges, showing why payment recovery belongs in the operating model rather than as an afterthought (Stripe, Chargeflow customer case study).

Payment processing with automated onboarding means using a workflow system to move a merchant from application through approval and activation before that merchant begins accepting customer payments. Merchant onboarding and payment processing are connected, but they are not the same operation.

In 2026, Stripe explained that a payment facilitator may aggregate businesses under one master merchant account, while later payment processing covers functions such as authorization, settlement, and fraud management (Stripe, Payment Industry Ecosystem Explained). That distinction prevents a common design mistake: treating an onboarding workflow as though it were the transaction-processing engine.

The automated layer handles predictable coordination work around the application. It can create a contact, attach the merchant’s submitted details, assign an outreach tier, request missing documents, send reminders, create reviewer tasks, record status changes, and start activation steps after approval.

Think of it as an operational state machine. A state machine is simply a controlled list of allowed statuses and transitions. A merchant might move from Submitted to Information Missing, then to Under Review, Approved, Rejected, or Exception Review. Each transition should have a trigger, an owner, and a recorded timestamp.

The workflow must also know when not to continue. An incomplete tax identifier should stop the review route. A rejected application should never reach invoice creation. An already approved merchant should not be re-enrolled because someone uploaded the same spreadsheet again.

The processor or acquiring environment still performs the work tied to accepting and moving money. That includes evaluating payment requests, communicating with card networks or banking rails, authorizing or declining transactions, settling funds, handling disputes, and applying transaction-level fraud controls.

The onboarding system may send approved merchant details into that environment through an API, webhook, or controlled staff handoff. It should record the resulting processor account identifier and activation status, but it does not replace the processor’s ledger, authorization logic, or settlement controls.

The practical boundary is clear: onboarding prepares and activates the merchant account; payment processing handles the merchant’s later customer transactions.

Payment processing with automated onboarding works by treating every merchant as a record that moves through explicit stages, with each approved change triggering the next permitted task.

Photo by Christina Morillo on Pexels

In 2026, HighLevel documented workflow actions spanning contacts, communications, ownership, tasks, opportunities, and payments, with actions running sequentially after a triggering event (HighLevel, What Are Workflow Actions?). That action model is enough to coordinate onboarding, provided the underlying fields and status rules are designed before the workflow is switched on.

GoHighLevel is a customer relationship management and workflow platform that can store contacts, manage pipeline records, run conditional rules, and coordinate follow-up. The application can enter through a native form, an integration, an API request, or a controlled import.

The entry event should create or update the merchant contact without assuming that a matching email address always represents the same application. A returning owner may apply for another business. A single business may have several authorized contacts. The application itself therefore belongs in an opportunity or application record, while the person’s reusable details belong on the contact.

At intake, the workflow should validate the fields required for routing. Missing information should not be represented as an empty value that later looks valid. It should produce a visible Information Missing state, assign an owner, and create a task explaining what is absent.

The entry step should also record the source, submission timestamp, consent basis, external application identifier, and the version of the form used. Those details become important when a merchant disputes a message or staff need to reconstruct why a particular route ran.

The outreach tier decides how the merchant is contacted, not whether the merchant is approved. A tier might be based on lead source, current processing volume, requested service, urgency, assigned representative, or a previously uploaded segment.

The routing logic should use explicit field values rather than loosely interpreted tags. Tags are useful for visibility and broad workflow membership, but a structured field such as Outreach Tier is easier to validate, report on, and change without leaving conflicting labels behind.

A dependable branch checks whether the tier is present, whether the contact can legally receive the selected communication, whether an owner has already started a conversation, and whether the application status still permits outreach. The branch should stop when a merchant replies, books a meeting, withdraws, or enters formal review.

This is where many implementations break. They correctly assign a tier but forget that the tier can change. The workflow needs a defined response when an owner upgrades a record, when a merchant submits a newer application, or when another system overwrites the field.

The communication sequence should begin with the core instruction in each step: send the right message, wait for the right event, and stop immediately when the record changes state. A sequence that keeps sending after a reply is not merely annoying; it tells the merchant that the company’s systems do not share context.

Email and SMS actions should reference verified contact fields and approved templates. Every message event should write back a send status or expose it through workflow history. Failed delivery should create an exception instead of silently advancing the merchant as though contact occurred.

Human tasks belong inside the same lifecycle. When a merchant replies with a complex question, the workflow can assign the account owner and suspend automated outreach. When documents arrive, it can notify the reviewer and move the application to a queue. When no response arrives, it can close the outreach route according to company policy rather than running indefinitely.

CogWorkLabs uses this same state-driven pattern in onboarding and billing builds: communication actions can run automatically, but every stop condition and ownership transfer is visible in the merchant record.

Approval should trigger a controlled activation route, not a vague “completed” status. The route should record who approved the application, when the decision occurred, which processor account was created, whether credentials were issued, and whether the merchant is ready to transact.

Only after those requirements are satisfied should billing setup begin. The workflow can create an invoice, apply the agreed billing cadence, select the customer payment method, store the invoice or subscription identifier, and notify the responsible staff member if creation fails.

The critical guard is idempotency. Idempotency means that repeating the same request does not create duplicate work. The workflow should use a stable approval or billing key so that a repeated webhook, manual retry, or duplicate status update cannot create another recurring invoice for the same agreement.

Approval, activation, and billing are therefore separate states even when they happen close together. Keeping them separate makes it possible to see whether a merchant is approved but not activated, activated but not billed, or billed with a failed payment method.

The workflow must track enough structured information to explain where every merchant is, who owns the next action, and whether billing has been created safely.

Photo by alleksana on Pexels

In 2026, HighLevel documented two custom-field scopes—contact and opportunity—so person-level details can remain separate from application-level values used in pipelines, forms, workflows, and reporting (HighLevel, How to Use Custom Fields). That separation is the foundation of a clean data model.

Contact fields should hold information that remains true across interactions: name, business email, phone number, communication consent, preferred channel, and assigned relationship owner. Merchant or opportunity fields should hold facts about the specific application: legal business name, application identifier, requested product, submission source, current review state, and processor account reference.

Sensitive information should not be copied into a general-purpose CRM merely because the workflow can store it. Keep regulated identity documents, card data, bank details, and underwriting evidence inside approved systems. The CRM can store a document-status value or secure reference without duplicating the underlying material.

The workflow also needs a reliable matching strategy. Email alone may be insufficient. Business identifiers, external application IDs, or a controlled combination of fields can help distinguish a revised application from an accidental duplicate.

A routing field should have a closed set of permitted values. Free-text statuses such as “waiting on stuff” or “John checking” are difficult to branch on and impossible to measure consistently.

Useful application states include intake, missing information, outreach active, merchant responded, review pending, exception review, approved, rejected, activation pending, active, and billing exception. The exact labels may differ, but their meaning and allowed transitions should be documented.

Ownership should also be explicit. Store the account owner, current task owner, and approval authority separately when those roles differ. A merchant can have a relationship manager while a risk analyst owns the review and a billing specialist owns an invoice exception.

Every meaningful transition should record its timestamp. Current status tells you where the merchant is now; transition timestamps tell you how long each stage took and where queues are forming.

Billing fields should connect the commercial agreement to the generated financial record. Store the billing start condition, cadence, amount source, invoice template, external invoice identifier, payment status, retry state, and exception owner.

Do not use a simple Invoice Created checkbox as the sole control. A checkbox cannot explain which invoice was created, whether the request succeeded, whether the customer has a valid payment method, or whether a later retry produced a duplicate.

In 2026, HighLevel documented that Execution Logs and Enrollment History show how individual contacts progressed, which actions ran, and where errors occurred (HighLevel, Improved Execution Logs and Enrollment History). Those logs should complement, not replace, business-level audit fields. Platform logs explain workflow execution; the merchant record should still expose the latest operational state.

People still need to review identity matches, business legitimacy, underwriting exceptions, and any decision that carries regulatory or financial authority.

In 2022, Signicat’s survey of 7,600 European consumers found that 38% had abandoned a financial application because they lacked suitable identity credentials, while 30% described applications as complicated and 21% cited application time, excessive personal information, or changing their mind (Signicat, The Battle to Onboard 2022). The age of the study should be considered, but the findings still illustrate why verification design affects both risk control and completion.

Automation can request documents, validate that required fields are present, send data to an approved verification provider, and route the returned status. It should not assume that a possible match is a confirmed result.

Names, addresses, business registrations, and identity records often contain variations. A screening response may be incomplete, ambiguous, or associated with another entity. The workflow should place those results into an exception state and give the reviewer the evidence needed to investigate.

Data minimization matters here. Collect only what the onboarding and compliance process requires, store it in the correct system, and give access only to roles with a legitimate need. A CRM status can say Verification Pending without exposing the underlying identity document to every sales user.

Underwriting evaluates whether the payment company is willing and permitted to support the merchant’s business model, expected volume, geography, ownership structure, and risk profile. Automation can assemble the file and enforce routing rules, but it cannot turn unclear evidence into a defensible decision.

High-risk categories, unusual processing patterns, mismatched ownership information, and unresolved screening results should produce a review queue. The queue needs an owner, reason code, supporting references, and escalation route.

In its merchant-screening guidance, Visa states that acquirers should investigate possible matches and make the acceptance decision after further investigation rather than treating the automated result as final (Visa, Merchant Screening Service). That is the right model for the entire workflow: machines organize evidence and enforce procedure; authorized people decide the exceptions.

Approval must identify the responsible person or authorized system, the decision timestamp, the policy or queue used, and any conditions attached to the decision. A generic status change made by an unrestricted user is not enough.

Permissions should prevent outreach staff from granting underwriting approval and prevent billing workflows from interpreting a draft status as a final decision. When an approval is reversed, the system should record the new state without erasing the earlier decision.

The audit record should answer a practical question: could an independent reviewer reconstruct what information was available, which checks ran, who made the decision, and what happened next? If not, the workflow is moving records without an independent reviewer reconstruct what information was available, which checks providing governance.

Three practical workflows show how automation can reduce coordination delay without pretending that every merchant or payment failure follows the same path.

Photo by Kindel Media on Pexels

In Stripe’s Mangomint customer case study, payment onboarding time fell by 64%, from approximately 14 days to fewer than five days (Stripe, Mangomint customer case study). That is a scoped vendor case study, not a universal forecast, but it shows what can happen when account creation and onboarding handoffs are redesigned together.

Before automation, the application moves through inboxes. A salesperson receives the form, copies details into the CRM, asks operations whether documents arrived, and messages the reviewer for an update. The merchant receives inconsistent follow-up because each person sees a different part of the process.

After automation, the application moves through states. Submission creates the contact and opportunity, checks required routing fields, records consent, assigns an owner, and places missing information into a visible queue. When the merchant supplies the requested material, the reviewer receives a task and the outreach route stops.

The workflow does not auto-approve the merchant. It ensures the reviewer receives a complete, organized case and that the resulting decision starts the correct downstream path.

A useful guard is to make every transition conditional on the current state. A late document webhook should not reopen an application that has already been rejected. A duplicate form should not create another active opportunity unless the matching rule determines that it represents a separate business or application.

Before automation, an uploaded file becomes an uncontrolled campaign. Staff import rows, apply labels manually, send batches, and later discover that some merchants had already replied, opted out, or entered review through another route.

After automation, the upload becomes a governed intake event. Each row is matched against existing contacts and applications. Valid records receive an outreach-tier value, source identifier, import timestamp, and assigned owner. Invalid records enter an exception list rather than a communication sequence.

The workflow then checks consent, contact validity, application status, and existing conversations before sending anything. A reply pauses the sequence and creates a task. A status change to review pending stops sales outreach. An opt-out blocks further messages across every related branch.

Volume alone does not prove quality. Stripe’s Booster case study reported that nearly 2,000 school accounts were onboarded in three weeks and that the connected-account total reached 4,000 by April 2024 (Stripe, Booster customer case study). The relevant lesson is not that every payment company should copy those numbers. It is that high-volume onboarding depends on consistent account creation, status visibility, and exception handling.

Before automation, approval and billing are separate staff memories. An account may be active while someone still needs to create the recurring invoice, confirm the start date, attach the correct pricing, and check whether a valid payment method exists.

After automation, approval creates a billing obligation with controls. The workflow checks the final approval state, billing agreement, activation status, existing invoice identifier, and payment method condition. It then creates the recurring invoice or routes the record to a billing exception.

The system should never derive the amount from an unvalidated free-text note. It should use an approved pricing field, contract reference, or invoice template selected during review.

Failed creation must remain visible. A merchant marked active with no invoice identifier should appear on an exception report. A repeated approval event should reuse the same idempotency key rather than producing another subscription. A cancellation or rejection should stop future billing according to the company’s policy while preserving the audit trail.

Automated onboarding matters because it reduces the time merchants spend waiting between departments and makes post-approval revenue tasks visible rather than assumed.

In 2024, Recurly estimated that inadequate failed-payment and involuntary-churn management could expose subscription companies to $129 billion in losses during 2025 within a $1.5 trillion industry; the estimate used an average 8.6% revenue lift observed among businesses using its churn-management tools (Recurly, Failed-Payment Analysis). The estimate is vendor-derived, but it demonstrates why onboarding design must continue through recurring payment recovery.

The workflow can create the merchant record and assign the initial owner as soon as a valid application arrives. Staff no longer need to wait for a spreadsheet to be reviewed or an inbox to be forwarded before the merchant receives an acknowledgement.

Speed should not mean sending every possible message immediately. The system should choose the correct channel, respect consent, and show the merchant what information is still required. A fast but confusing response can increase support work without improving completion.

Activation also becomes measurable. Once approval is recorded, the workflow can start account provisioning, credential delivery, training tasks, and billing setup. If activation stalls, the responsible owner can see the exact missing condition rather than a generic “approved” label.

Consistency comes from shared stop conditions, not from sending more reminders. Every outreach branch should stop when the merchant replies, opts out, enters review, is rejected, or becomes active.

Templates can keep the required information consistent while still allowing the owner to step in. The workflow should preserve the conversation context and avoid restarting a sequence merely because a tag was reapplied.

Automated merchant onboarding software for payment processors with tiered outreach and recurring invoice workflows.

Escalation rules make silence visible. A merchant that has not responded can move to a review queue, a lower-frequency route, or a closed state according to policy. The important point is that the outcome is intentional and recorded.

Billing becomes safer when the approval event creates a structured obligation rather than an informal request to finance. The system can verify the billing fields, create the invoice, store its external identifier, and assign any exception.

Recurring payments also need a recovery path. A failed charge is not the same as a cancelled customer. The workflow should distinguish temporary payment failure, expired credentials, deliberate cancellation, disputed charges, and an account that should no longer be billed.

Connecting those states prevents two costly mistakes: leaving an active merchant unbilled and continuing to bill a merchant whose agreement has ended.

A controlled automated lifecycle removes repetitive coordination while preserving the human decisions that carry risk or approval authority.

| Lifecycle point | Manual workflow | Controlled automated workflow |

|---|---|---|

| Application intake | Staff copy form or spreadsheet data into several records. | Intake creates or updates the contact and application using defined matching rules. |

| Missing information | Staff notice gaps during review and send ad hoc requests. | Validation creates an exception state, owner, and document request. |

| Tiered outreach | Campaign lists are built manually and may ignore current status. | Routing checks tier, consent, ownership, replies, and application state before sending. |

| Review handoff | Reviewers receive incomplete context through email or chat. | The record contains required fields, references, history, and a visible review task. |

| Approval | A status is changed without clear authority or downstream checks. | Approval records the decision owner and starts only permitted activation steps. |

| Activation | Teams assume another department completed account setup. | Each activation requirement has a state, owner, and exception path. |

| Recurring billing | Finance creates invoices from notes or reminders. | Billing uses approved fields, checks for an existing invoice, and records the result. |

| Failure recovery | Failed sends, invoices, or payments are discovered late. | Execution errors and payment exceptions enter owned recovery queues. |

The strongest benefit is accountability. Every merchant has a current state, every state has an owner, and every failed handoff remains visible until someone resolves or closes it.

The workflow is working only when it improves merchant progress, billing outcomes, and exception control—not merely when it sends more messages.

In Stripe’s Chargeflow case study, automated recovery tools reclaimed 48% of revenue associated with failed charges (Stripe, Chargeflow customer case study). That figure belongs on a scorecard as a scoped case-study result, while each payment company should measure recovery against its own historical baseline.

Time to initial contact measures intake delay. Start the clock when a valid merchant application reaches the system and stop it when the first permitted acknowledgement or owner contact is recorded. Separate automated acknowledgements from genuine staff responses so the metric does not hide a slow human queue.

Time in missing-information status measures document friction. Track the interval from the first missing-field decision until the required information arrives or the application closes. Segment it by requested document type and outreach tier to find recurring blockers.

Unresolved exception age measures operational neglect. Every exception should have a created timestamp, owner, reason, and latest activity. A queue can remain small while still containing dangerously old records, so average volume alone is not enough.

Application completion rate measures whether merchants reach a reviewable state. Define the denominator carefully. Submitted forms, validated applications, and sales-qualified opportunities are different populations and should not be mixed.

Approval-to-activation time measures post-decision delay. Start when authorized approval is recorded and stop when the merchant account is ready for the intended processing activity. This reveals whether the bottleneck sits in underwriting or in provisioning after underwriting has finished.

Activation rate measures whether approved merchants become usable accounts. An approval that never reaches activation should appear as a separate operational loss, not as a completed onboarding success.

Segment conversion metrics by source, tier, assigned owner, merchant type, and exception reason. A healthy overall rate can conceal a failing upload source or a tier that receives the wrong follow-up.

Invoice creation success measures whether approved obligations became valid billing records. The workflow should compare merchants eligible for billing with merchants holding a confirmed invoice or subscription identifier.

Initial payment success measures whether billing began correctly. A failed initial charge may indicate an invalid payment method, incorrect start condition, missing mandate, or configuration error. It should not be grouped blindly with later recurring failures.

Failed-charge revenue recovery measures what the recovery process actually reclaimed. Track recovered value, unrecovered value, recovery method, and time to recovery. A high retry count with little recovered revenue may create support friction without producing a useful outcome.

Billing exception age measures how long money-related errors remain unresolved. Segment failures by invoice creation, payment method, gateway response, cancellation conflict, and manual hold.

Duplicate-contact rate measures intake control. Count records that required merging, suppression, or manual review because matching logic could not determine whether the merchant already existed.

Duplicate-work rate measures idempotency failures. Examples include repeated invoice creation, duplicate tasks, restarted outreach, or repeated processor-account requests for the same event.

Manual-review rate measures where automation reaches its boundary. A high rate is not automatically bad; it may reflect appropriate risk controls. The useful question is whether the review queue contains the right cases and enough context for a timely decision.

Workflow error rate measures technical reliability. Group failures by action, integration endpoint, authentication issue, missing field, invalid state transition, and provider response. The error report should lead to an owner and recovery action, not simply a red badge in a dashboard.

A production workflow should stop safely, preserve context, and create an owned exception whenever it cannot prove that the next action is valid.

In 2026, HighLevel documented that failed recurring-invoice auto-payments receive two additional retry attempts spaced 24 hours apart, with notifications sent to the customer and account user (HighLevel, Auto Payments in Recurring Templates). That documented behavior is useful, but the surrounding workflow still needs to decide what happens after recovery fails.

Block uncertain duplicates before communication or billing. The matching process should compare stable identifiers and route ambiguous results for review. Automatically merging records based on a shared phone number can combine unrelated contacts; automatically creating every row can produce conflicting applications.

Represent missing information as a state. Do not let blank required fields pass into later branches. Create an exception reason, assign an owner, and record what is needed.

Preserve the original submission. Corrections should update the working record while retaining enough history to explain what changed. Overwriting every value without history makes disputes and audit review harder.

Stop the sequence when delivery or consent is uncertain. A failed email, invalid phone number, or opt-out should prevent later messages on the affected channel. The record should show the failure reason and the route available for recovery.

Reject stale transitions. An outreach workflow that started earlier should not move a merchant back to Contacted after a reviewer has already marked the application Approved or Rejected. Every transition should confirm the current state before writing the next state.

Resolve ownership conflicts explicitly. If an import assigns a new owner while an active representative is handling the merchant, the workflow should follow a documented precedence rule rather than silently replacing the owner.

Separate creation failure from payment failure. An invoice that was never created needs a technical or data correction. A valid invoice with a declined payment needs a payment-recovery route. Combining them under Billing Failed hides the required action.

Record the external result before advancing. The workflow should not mark billing complete until the payment platform returns a usable invoice or subscription identifier.

Escalate exhausted recovery attempts. HighLevel’s documented recurring-payment behavior includes two additional retries at 24-hour intervals. When those attempts fail, the workflow should assign an owner, notify the merchant through an allowed channel, and prevent the account from disappearing inside an unresolved retry state.

Retry the failed action, not the entire lifecycle. Restarting the full workflow may resend messages, recreate tasks, or issue another invoice. The recovery route should resume from the failed step after confirming that earlier steps already succeeded.

Use stable idempotency keys. The key can be derived from the application, approval event, billing agreement, and intended action. Before creating anything, the workflow checks whether the corresponding external identifier already exists.

Keep retries observable. Record the attempted action, provider response, retry count, next eligible attempt, and final disposition. Staff should be able to distinguish a temporary failure under active recovery from a permanent exception awaiting a decision.

The practical next step is to map onboarding, tiered outreach, approval, activation, and billing as a single controlled lifecycle before building individual automations.

In 2026, HighLevel’s documentation showed that triggered workflows can coordinate contact updates, communications, ownership, tasks, opportunity changes, and invoice actions within the same platform. The remaining work is to define the states, permissions, stop conditions, and recovery rules that make those actions dependable.

When application records and monthly invoices keep falling out of sync, start by mapping the approval-to-billing handoff and the identifier that prevents duplicate creation. CogWorkLabs can help build that controlled lifecycle through its payment processing with automated onboarding service.

Awais Ahmad is a Senior RPA and Workflow Engineer at CogWork Labs. He builds production workflow automation with retries that actually retry, idempotency, and audit trails — turning brittle scripts into RPA that holds up at scale.

See the benefits of email automation for customer nurturing, from better segmentation and timely follow-up to clearer funnel tracking and stronger sales.

Learn how marketing automation real estate CRM systems capture, qualify, nurture, and route leads while keeping daily follow-up and deal stages organized.

See how mortgage marketing automation uses CRM triggers to run borrower and Realtor journeys, protect compliance, and measure results beyond clicks alone.